RFB Normative Instruction No. 2,290/2025 (“IN RFB No. 2,290/2025”), published on October 30, 2025, and effective as of January 1, 2026, introduced changes to the rules governing the identification and reporting of beneficial owners in Brazil. The regulation significantly expanded the scope of entities required to disclose who ultimately owns, controls, or benefits from their activities, in line with international standards for transparency and the prevention of financial crimes.

The e-BEF as the official channel.

The main operational change introduced by the regulation is the creation of the Digital Beneficial Owner Form (e-BEF), which now serves as the official channel for reporting beneficial owners to the Federal Revenue Service. Under the terms of Article 55-A, the system uses a pre-filled electronic form containing data already on file in the Federal Revenue Service’s systems (Article 55-A, Paragraph 4), which is directly integrated with the CNPJ registry. As a result, reporting the beneficial owner is no longer merely an ancillary obligation: individuals identified as beneficial owners are now included in the legal entity’s registration data with the CNPJ and integrated into the Federal Revenue Service’s Registration Portal.

The e-BEF must be filed centrally by the head office, with a digital signature from the entity and the beneficial owners registered with the CPF. For beneficial owners who are not residents of Brazil, the e-BEF must contain additional information, including: full name, date of birth, identity document or passport, country of tax residence with the respective Tax Identification Number (NIF), nationality, permanent residential address, and contact email. When there is a legal representative or attorney-in-fact in Brazil, this information must also be provided.

Concept of Beneficial Owner and Scope of Reporting Entities.

The general rule remains the identification of the individual who, directly or indirectly, owns, controls, or exercises significant influence over the entity. If no individual meets these criteria, those who manage the entity must be reported as beneficial owners.

Accordingly, the following are required to file the e-BEF: limited liability companies and privately held corporations domiciled in Brazil; entities and legal arrangements (trusts) domiciled abroad when required to register with the CNPJ; and civil and commercial partnerships, associations, cooperatives, and foundations.

Investment funds and offshore structures.

For investment funds, the obligations go beyond the e-BEF. Fund managers and financial institutions acting as distributors of shares on behalf of and at the direction of clients must submit information monthly to the Federal Revenue Service, via the Coleta Nacional system, including the identification of each shareholder, the type and number of shares, the value, and the respective distributor.

As for funds and other entities domiciled abroad, including legal arrangements (trusts), the beneficial owner rules also apply when registration with the CNPJ is mandatory. That is, when the entity holds assets or rights in Brazil or engages in legal acts or transactions that require such registration. There are, however, exceptions: global custodians are only required to provide information if the Federal Revenue Service expressly requests it, provided they do not have significant influence over an entity domiciled in the country.

Phased Filing of the e-BEF

The regulation provides for a phased implementation of the e-BEF filing obligation: simple or limited liability companies with revenue exceeding R$ 78,000,000.00 will be required to file starting January 1, 2027, and those with revenue exceeding R$ 4,800,000.00 will be required to do so as of January 1, 2028.

Important: limited liability companies that have at least one legal entity listed in the QSA are not eligible for the phased implementation and must file the e-BEF in accordance with Article 55-A, effective as of the rule’s entry into force.

State-owned companies, mixed-capital companies, publicly traded corporations and their subsidiaries, individual microentrepreneurs (MEI), and single-member companies are expressly exempt from these obligations.

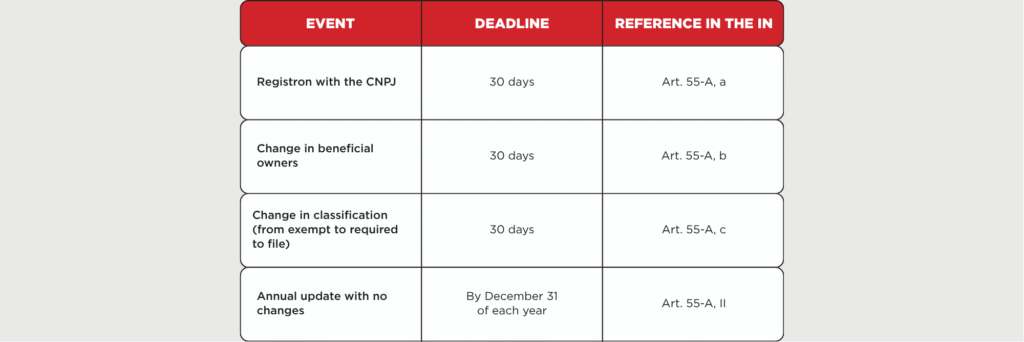

Filing deadlines.

Penalties for noncompliance.

In the event of noncompliance, any omission, inaccuracy, or delay in providing information via the e-BEF may result in the suspension of the CNPJ registration and the blocking of banking transactions. In both cases, the penalty is preceded by a formal notice granting a 30-day period to rectify the situation. Noncompliance also subjects the entity to a late filing fine.

Furthermore, the regulation provides for criminal liability for false information: anyone who submits false data through the e-BEF is, in theory, guilty of the crime of ideological falsehood, as provided for in Article 299 of the Penal Code.

To comply with the new regime, companies must map their corporate structure to identify the controlling individual, establish internal processes for updating registration information in cases of changes in control or ownership, ensure the annual filing of the e-BEF—even in years without changes—and retain supporting documentation for at least five years. Companies that have not yet mapped their corporate chain or that have complex structures should begin this process well in advance, as noncompliance may block banking transactions and prevent them from obtaining certificates of tax compliance.

Access the e-BEF here.

This content is provided for informational purposes only and does not constitute legal advice. The application of this information depends on the analysis of each specific case.