Recent developments in the Brazilian agribusiness capital markets have shifted the discussion regarding the sector’s financing instruments. For years, the Agribusiness Receivables Certificate (“CRA”) held a central position in the incentivized fundraising conducted by companies and other agents in the agroindustrial chain, particularly due to its securitization structure, the possibility of public distribution, and the tax treatment applicable to individual investors.

In recent months, however, the Rural Product Note with Financial Settlement (“CPR-F”) has taken center stage. Traditionally used as a bilateral rural financing instrument or as an underlying asset in securitization transactions, the CPR-F has also come to be structured as a debt instrument distributed directly to investors in the capital markets, including individual investors.

This trend gained visibility with the settlement, in August 2025, by B3, of the first public offering of CPR-F intended for the general investing public, issued by Klabin in the amount of R$1.5 billion, in a transaction coordinated by Itaú BBA and XP.[1]

Subsequently, new transactions involving public offerings of CPR-F further reinforced the perception that the instrument has come to occupy a distinct place in the agribusiness funding landscape.[2]

This shift is not merely the result of financial innovation or the pursuit of economic efficiency. It is also a direct result of regulatory developments. The changes introduced by the National Monetary Council (“CMN”), particularly through Resolution No. 5,118 of February 1, 2024 (“CMN Resolution 5,118”), later amended by Resolution No. 5,212, dated May 22, 2025 (“CMN Resolution 5,212”), restricted certain CRA structures and reinforced the need for effective alignment between the incentivized instrument, the beneficiary economic sector, and the use of the proceeds.

In this context, the public offering of CPR-F should not be understood as a natural substitute for the CRA in all situations. Rather, it is an alternative that now competes for market share in certain direct funding transactions, especially when the issuer is eligible to issue CPR-F but lacks collateral compatible with the new rules now applicable to CRA issuances, and when the transaction does not require the interposition of a securitization company, the creation of a segregated estate, or the pooling of a portfolio of credit rights.

The analysis, therefore, should not be based on an abstract opposition between CRA and CPR-F, but on the role each instrument plays in the financing structure. It is important to determine, in each case, which one best accommodates the nature of the funding, the issuer’s profile, the risk to be distributed to the market, and the regulatory requirements that now govern private agribusiness financing.

1. The CRA as an Agribusiness securization instrument

The CRA is a registered, freely transferable negotiable instrument representing a cash payment promise, linked to agribusiness credit rights. Its legal framework stems primarily from Law No. 11,076, of December 30, 2004, and Law No. 14,430, of August 3, 2022 (“Law 14,430”), which establishes the legal framework for securitization in Brazil and consolidates the rules applicable to securitization companies and receivables certificates.[3]

In the typical securitization structure, the securitization company acquires agribusiness credit rights and links them to the issuance of CRAs, which are subsequently distributed to investors in the capital markets. The transaction is formalized through a securitization indenture (termo de securitização), an instrument that defines the underlying assets and payment terms of the CRAs, the collateral and guarantees established, events of acceleration, and the other rules applicable to the transaction.[4]

[4]Law No. 14,430/2022, particularly Articles 22, 26, and 27, which address, respectively, the securitization indenture, the establishment of the fiduciary regime, and the segregated estate. [4]

In CRA issuances, the securitization company may establish a fiduciary regime over the credit rights, assets, and guarantees linked to the issuance, with the consequent creation of a segregated estate, pursuant to Law 14,430

The segregated estate is held by the securitization company but remains non-commingled with the company’s own assets and with the segregated estates of other issuances. This is an asset segregation mechanism designed to link the assets and cash flows of the transaction to payments to CRA holders and to the expenses of the respective issuance.

From an economic standpoint, the CRA is particularly efficient in structures involving credit portfolios, multiple debtors, the need for asset segregation, different classes or series of securities, subordination mechanisms, credit enhancements, or more sophisticated risk allocation arrangements.

On the other hand, when compared to direct funding through a public offering of CPR-F, the issuance of CRAs involves an additional layer of complexity and may entail higher costs, longer execution timelines, and greater structural sophistication.

2. CPR-F: From rural financing note to public funding instrument

The Rural Product Note was created by Law No. 8,929, of August 22, 1994 (“Law 8,929”), as a negotiable instrument representing a promise to deliver a rural product (“CPR”). Subsequently, the legislation began to allow for the financial settlement of the obligation represented by the note, giving rise to the CPR-F.[5]

[5]Law No. 8,929, of August 22, 1994, Art. 1; Law No. 10,200, of February 14, 2001; and Law No. 8,929, Art. 4-A, as subsequently amended. [5]

Unlike the physical CPR, where the principal obligation consists of the delivery of the rural product, the CPR-F is settled in cash, according to the price or index expressly provided for in the instrument. The obligation remains linked to the underlying rural product, but its fulfillment occurs through monetary payment, which has given the instrument greater flexibility for financial and structured transactions.

The modernization of the legal framework governing CPRs, particularly following the enactment of Law No. 13,986 of April 7, 2020 (the “Agribusiness Law”), was decisive in bringing them closer to the capital markets. Among the main innovations are the possibility of book-entry issuance, registration or deposit with an entity authorized by the Central Bank of Brazil, the expansion of eligible issuers, clearer rules governing the in rem collateral attached to the note (garantias cedulares), and greater standardization of the note’s circulation.[6]

[6]Law No. 13,986, of April 7, 2020; Law No. 14,421, of July 20, 2022; Law No. 8,929/1994, Articles 2, 3, 8, 10, and 12. [6]

These changes increased the legal and operational certainty of the CPR-F. The instrument is no longer perceived solely as a bilateral rural financing tool and is increasingly being used in structured transactions, either as the underlying asset of a CRA or as a direct funding instrument for eligible issuers.

The public offering of the CPR-F represents a significant turning point in the instrument’s trajectory. The instrument, previously associated with bilateral rural financing transactions or with serving as the underlying asset of securitization structures, is now distributed directly to investors in the capital markets, subject to the applicable rules of CVM Resolution No. 160, dated July 13, 2022 (“CVM Resolution 160”). Unlike the CRA, in which the securitization company acquires agribusiness credit rights and links them to the issuance of certificates, the public offering of CPR-F enables the issuer of the note itself to raise funds directly.

This feature may represent a significant advantage for certain issuers, particularly in terms of structural simplicity and potential cost savings. At the same time, it requires additional attention to the issuer’s credit quality, the appropriate allocation of proceeds, the regularity of the CPR-F issuance, the adequacy of collateral (where applicable), and the quality of information provided to investors.

From a tax perspective, the instrument’s attractiveness also stems from the treatment afforded to income earned by individuals from CPR-F, subject to applicable legal requirements.[7]

[7]Law No. 11,033, of December 21, 2004, Art. 3, V, which provides for an income tax exemption on the income generated by CPR-F, subject to applicable legal requirements.[7]

3. The role of regulation: Restrictions on CRAs and the opening for CPR-Fs

The recent expansion of public offerings of CPR-F should be read in conjunction with the regulatory restructuring of the incentivized instruments market. CMN Resolution 5,118 established new rules for collateral eligible to back CRAs and Real Estate Receivables Certificates (“CRI”), seeking to reinforce the alignment of these instruments with the economic sectors that justify the incentivized treatment.[8]

[1]CMN Resolution No. 5,118, dated February 1, 2024, which provides for the collateralization of the issuance of Agribusiness Receivables Certificates and Real Estate Receivables Certificates.

In the case of CRAs, the rule restricted certain structures backed by debt securities of issuers, debtors, co-debtors, or guarantors whose primary sector of activity was not agribusiness. CMN Resolution 5,212 broadened this approach by extending restrictions previously applicable to publicly held companies to privately held companies and other legal entities that do not operate significantly in agribusiness or in the real estate sector, as applicable.[9] [9]

The regulatory objective is clear: to prevent incentivized instruments from being used by issuers whose primary economic activity is not sufficiently related to the beneficiary sector. In this regard, the regulation now requires greater consistency between the tax benefit, the underlying assets backing the transaction, and the economic use of the proceeds.

This new environment has reduced the scope for certain “CRA by destination” structures, in which companies with only partial or indirect involvement in agribusiness sought to access the CRA market based on the allocation of proceeds to activities related to the sector. For these issuers, the eligibility analysis has become more rigorous.

It is at this point that the public offering of CPR-F gains relevance. In certain situations, companies facing doubts or restrictions regarding market access through a CRA public offering may find the CPR-F to be an alternative for direct fundraising, provided they are authorized to issue such instrument and the transaction complies with the legal requirements applicable to the CPR-F, including those regarding the link to a rural product, the allocation of proceeds, and the registration of the note.

The CPR-F, however, should not be treated as a regulatory shortcut: a public offering of the instrument does not eliminate the need for economic, documentary, and informational consistency in the transaction. On the contrary, the broader the distribution to the market, the greater the importance of adequate risk disclosure, governance of the offering, and clarity regarding the use of proceeds.

The initial consolidation of this market confirms the relevance of the trend. According to data released by B3, public CPR issuances targeting individual investors have totaled R$6 billion since August 2025, distributed across 14 issuances, with 4 million units and more than 26,000 investors. [10]

4. CRA E CPR-F: Competing or complementary instruments

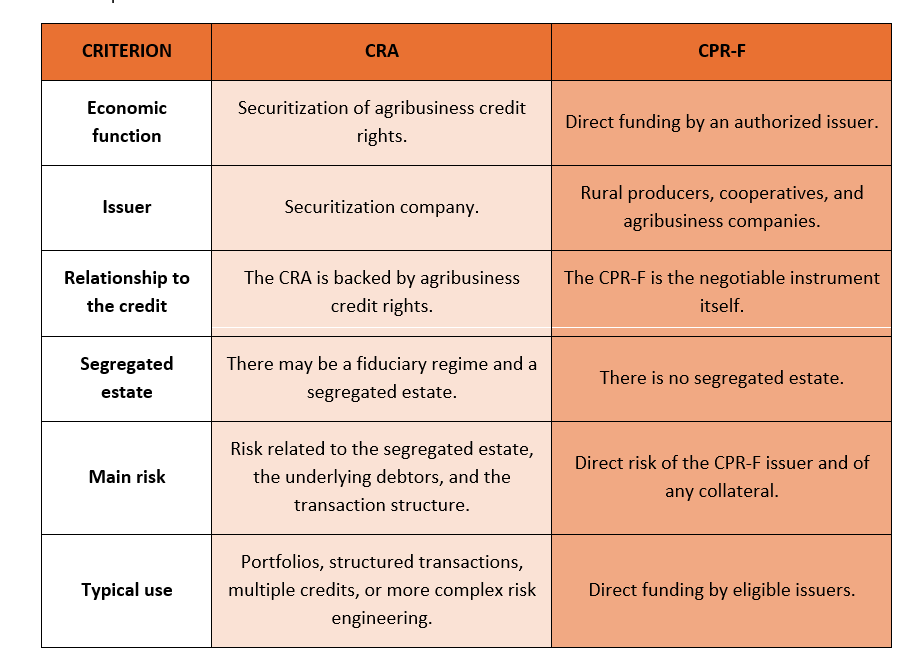

The relationship between CRA and CPR-F is best understood through the economic function performed by each instrument.

The CRA is, essentially, a securitization instrument. It allows the transformation of agribusiness credit rights into securities distributed to investors, through the interposition of a securitization company and, when established, with the additional protection of the fiduciary regime and the segregated estate.

The CPR-F, in turn, is the negotiable instrument itself, issued by the authorized agent, with a financial settlement obligation. When publicly distributed, it allows for direct fundraising from the market, without the need for securitization. The investor assumes, more immediately, the risk of the CPR-F issuer and of any collateral established, without the structural layer of the segregated estate typical of the CRA.

The choice between the instruments therefore depends on the intended structure.

In fragmented transactions involving multiple credit claims, the need for asset segregation, varying risk levels, or third-party origination, the CRA tends to offer significant advantages. Conversely, in direct fundraising by eligible issuers with clearer corporate credit, proceeds earmarked for agribusiness, and less need for securitization engineering, the CPR-F may represent an efficient alternative.

Even so, the public offering of CPR-F does not fully replicate the regulatory dynamics of the CRA. Depending on the issuer’s profile and the intended target investor base, the offering may not fall within the automatic registration provisions of CVM Resolution 160, in which case it would have to be submitted to the ordinary procedure, with prior review by the CVM. For issuers not registered as publicly held companies (companhias abertas) seeking to access a broad investor base, this aspect is particularly relevant, as it may reduce the time and cost efficiencies that, in theory, would justify choosing a direct offering.

[11].

The comparison between CRA and CPR-F can be summarized as follows:

This distinction is essential to avoid a simplistic interpretation of recent developments. The public offering of CPR-F does not eliminate the CRA. It merely creates a new funding channel for situations in which securitization is not necessary, not possible, or not the most efficient structure.

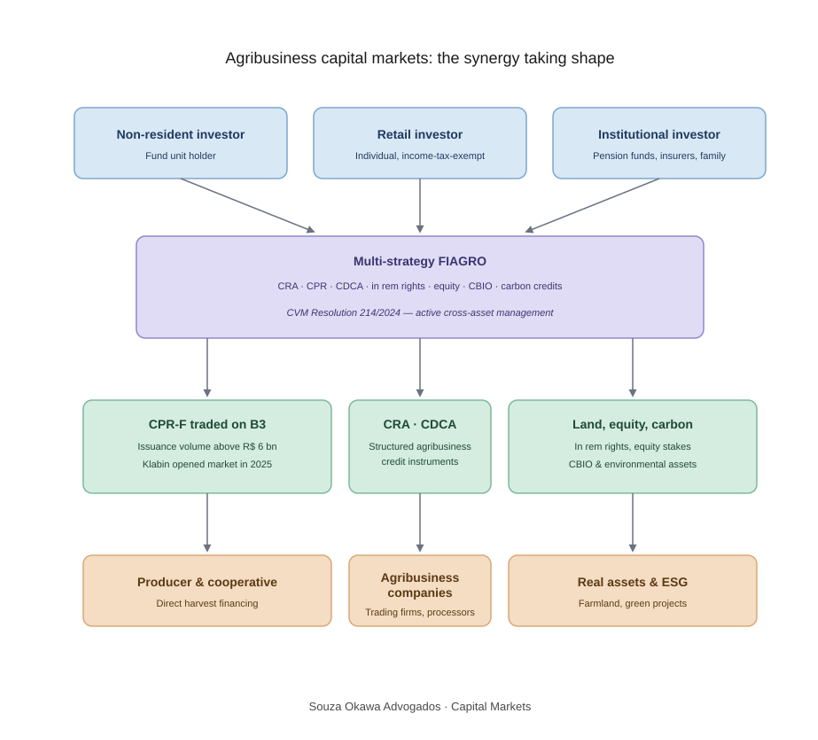

5. CPR-F, CRA, Multi-strategy FIAGRO and institutional capital

The flow of capital into Brazilian agribusiness, including from institutional and non-resident investors, has become more sophisticated, going beyond direct investment in productive assets, companies, or specific projects. A combined reading of two recent regulatory developments helps explain this new landscape: on the one hand, the consolidation of the public offering of CPR-F as a direct fundraising instrument; and on the other, the final regulation of the Investment Fund in Agro-Industrial Production Chains (“FIAGRO”) and the opening for multi-strategy structures.

The first development concerns the consolidation of the public CPR-F as a direct fundraising instrument in the capital markets. Beginning with the first public offering transactions, the CPR-F came to occupy its own space alongside the CRA, no longer merely as a bilateral asset or as collateral for securitization, but as an instrument eligible for public distribution to investors, including the general investing public. This trend was accelerated, in part, by the restrictions introduced by CMN Resolution 5,118 in the CRA market.

The second development lies in FIAGRO. CVM Resolution No. 214, dated September 30, 2024 (“CVM Resolution 214”), added Regulatory Annex VI and Supplements O, P, and Q to CVM Resolution No. 175, dated December 23, 2022, establishing specific rules for FIAGROs.[12] The new framework took effect on March 3, 2025, and consolidated the possibility of structures with investment policies capable of combining different categories of agribusiness assets, subject to the classification and subsidiary application rules set forth in the regulation.

In practice, this flexibility positions the multi-strategy FIAGRO as an active allocation platform in agribusiness. The fund can, in theory, combine exposure to credit, land, equity interests, and environmental assets, without being restricted to a single economic category. This structure tends to be particularly relevant for institutional and non-resident investors seeking diversified exposure to the Brazilian agro-industrial chain through a vehicle regulated by the CVM, with professional management, independent governance, and the transparency rules applicable to investment funds.

The synergy with the public offering of CPR-F is evident. A multi-strategy FIAGRO can act as an institutional anchor in public CPR-F issuances originated by medium-sized producers, cooperatives, or agribusiness companies, calibrating exposure by harvest, region, crop, or segment, incorporating professional credit analysis while simultaneously holding positions in CRAs, in rem rights over rural real estate, equity stakes in companies within the chain, and agribusiness-related environmental assets.

This combination does not turn the FIAGRO into a substitute for the CRA, nor the CPR-F into a universal substitute for securitization. The point is different: the regulation has created instruments that can be structured in a more sophisticated manner:

- I. – the CPR-F offers a direct funding route;

- II. – the CRA preserves the function of securitization and asset segregation; and

- III. – the multi-strategy FIAGRO can function as a vehicle for allocation, origination, and diversification within the same economic chain.

The regulatory framework is now in place. The instruments exist and are growing at a rapid pace. The next chapter in Brazil’s agribusiness capital markets is likely to depend less on the creation of new instruments and more on the combination of legal structuring, origination capabilities, credit analysis, and distribution governance.

6. Key considerations in structuring CPR-F public offerings

The expansion of CPR-F public offerings is likely to bring new opportunities, but also new points of attention for issuers, underwriters, investors, and legal advisors.

The first point is the issuer’s eligibility. The CPR-F may not be issued by just any company interested in accessing the incentivized market. It is necessary to verify whether the issuer qualifies as a legally authorized party and whether its economic activity permits the issuance of the note in accordance with Law 8,929.

The second point is the link to a rural product. Although the CPR-F is settled financially, its structure must adhere to the legal framework of the CPR, including the identification of the rural product, the index or criterion for calculating the amount due, and the other essential terms of the note.

The third point is the allocation of proceeds. In public offerings, clarity regarding the use of the proceeds raised is relevant not only economically but also from a regulatory and informational standpoint. The allocation must be consistent with the issuer’s business and with the legal and economic basis for the issuance.

The fourth point is the distribution regime. The private placement of CPR-F should not be confused with its public distribution. Whenever there is a public offering, including to the general investing public, the rules of CVM Resolution 160 must be observed, including, where applicable, submission to the ordinary registration procedure.

The fifth point is the absence of a segregated estate. Unlike the CRA, the CPR-F does not, in and of itself, provide the asset segregation typical of securitization. This does not prevent the creation of in rem collateral, but it alters the nature of the risk assumed by the investor. Credit analysis now falls more directly on the issuer, on its payment capacity, on its assets, and on any collateral provided in connection with the transaction.

Finally, secondary liquidity will be a key factor in the consolidation of this market. The CRA is already a familiar instrument to investors and has a longer track record of trading on organized markets. The CPR-F is still in the early stages of building a track record, standardization, and investor familiarity.

7. Final Considerations

The recent regulation has not transformed the CPR-F into a universal substitute for securitization. What we are seeing is a reorganization of the alternatives available for the private financing of agribusiness.

The CRA remains central to transactions that require securitization, a segregated estate, the pooling of receivables, and more complex risk allocation structures. Its role remains particularly relevant for connecting investors to the cash flow of agribusiness credit rights portfolios, through the interposition of a securitization company and the legal protection of the fiduciary regime.

The CPR-F, on the other hand, opens a direct funding channel for eligible issuers, with the potential to reduce structural complexity and issuance costs in transactions in which securitization is not possible or necessary. Its rise reflects both the legal modernization of the CPR and the effect of the new regulatory restrictions applicable to the CRA.

The multi-strategy FIAGRO adds an additional layer to this trend. By allowing the regulated combination of different exposures to agribusiness, it can serve as a vehicle for institutional allocation in credit transactions, rural real estate assets, equity interests, and environmental assets, including in connection with public offerings of CPR-F.

The choice between CRA and CPR-F should be made on a case-by-case basis, based on the nature of the issuer, the use of proceeds, the type of risk to be distributed to the market, the need (or lack thereof) for a segregated estate, the target investor base of the offering, and the economic efficiency of the structure.

In summary, the new landscape does not necessarily pit the CRA against the CPR-F. It calls for a more precise analysis of the function of each instrument. The regulation has reshaped the market by restricting structures less suited to agribusiness and, at the same time, has created room for the CPR-F to establish itself as a relevant alternative for direct fundraising.

For issuers and investors, the consequence is clear: the sophistication of agribusiness financing will depend not only on the choice of instrument, but on the coherence between the legal structure, the economic activity, and the risk actually assumed.

—

[1] B3. “B3 Facilitates the First Public CPR Offering.” São Paulo, Aug. 25, 2025. 2025. The article reports that Klabin’s R$1.5 billion offering was coordinated by Itaú BBA and XP.

[2]CNN Brasil. “Klabin announces issuance of up to R$1.75 billion in CPR-Fs.” March 28, 2026. The article reports that Klabin’s second CPR-F issuance would be targeted at the general investing public, under an automatic registration procedure.

[3] Law No. 11,076, of December 30, 2004, particularly Articles 23 and 36; and Law No. 14,430, of August 3, 2022, particularly Articles 18 et seq..

[4] Law No. 14,430/2022, particularly Articles 22, 26, and 27, which address, respectively, the securitization indenture, the establishment of the fiduciary regime, and the segregated estate.

[5] Law No. 8,929, of August 22, 1994, Art. 1; Law No. 10,200, of February 14, 2001; and Law No. 8,929, Art. 4-A, as subsequently amended.

[6] Law No. 13,986, of April 7, 2020; Law No. 14,421, of July 20, 2022; Law No. 8,929/1994, Articles 2, 3, 8, 10, and 12.

[7] Law No. 11,033, of December 21, 2004, Art. 3, V, which provides for an income tax exemption on the income generated by CPR-F, subject to applicable legal requirements.

[8] CMN Resolution No. 5,118, dated February 1, 2024, which provides for the collateralization of the issuance of Agribusiness Receivables Certificates and Real Estate Receivables Certificates.

[9] CMN Resolution No. 5,212, dated May 22, 2025; Ministry of Finance. “National Monetary Council refines criteria for the issuance of CRAs, CRIs, and CDCAs.” May 22, 2025. Available at: https://www.gov.br/fazenda/pt-br/canais_atendimento/imprensa/notas-do-cmn/2025/maio/conselho-monetario-nacional-aprimora-criterio-para-emissao-dos-certificados-cras-cris-e-cdcas

[10] B3 Bora Investir. “Public CPR issuances on B3 total R$6 billion.” Feb. 19, 2026. 2026. According to the publication, the volume was raised through 14 issuances, which totaled 4 million units and attracted more than 26,000 investors. Available at: https://borainvestir.b3.com.br/tipos-de-investimentos/renda-fixa/emissoes-de-cprs-publicas-na-b3-somam-r-6-bilhoes/

[11] CVM Resolution 160, Art. 25, § 2.

[12] CVM Resolution No. 214, dated September 30, 2024, which added Regulatory Annex VI and Supplements O, P, and Q to CVM Resolution No. 175/2022, containing specific rules for FIAGROs. The regulation was published in the Official Gazette on Oct. 1, 2024, and amended in the Official Gazette of Feb. 14, 2025. 2025.

[13] CVM Resolution No. 175/2022, Regulatory Annex VI, Articles 2 and 14. Article 14 permits, among other assets, in rem rights over rural real estate, equity interests, financial assets, debt securities and securities issued by entities in the agribusiness production chain, credit rights, CRA and other securitization instruments, agribusiness carbon credits, and CBIO.

This content is provided for informational purposes only and does not constitute legal advice. The application of this information depends on the analysis of each specific case.