On April 30, 2026, the federal government published the sectoral regulations for the Social Contribution on Goods and Services (CBS) and the Tax on Goods and Services (IBS):

- Decree No. 12,955/2026: regulates the CBS and, in its Book I, establishes the rules common to both the CBS and the IBS.

- CGIBS Resolution No. 6/2026: regulates the IBS, which falls under the jurisdiction of the states, the Federal District, and the municipalities.

With the publication of these regulations and the formalization of the “common part” through Joint Ordinance MF/CGIBS No. 7/2026, the four-month period provided for in Art. 3 of Joint Act RFB/CGIBS No. 1/2025 has begun.

ATTENTION:

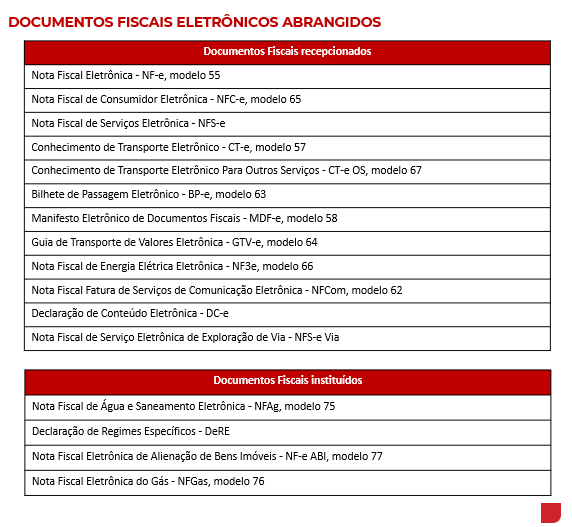

Thus, as of August 1, 2026, it becomes mandatory to fill in the new IBS and CBS fields in electronic tax documents.

Art. 3 of Joint Act RFB/CGIBS No. 1/2025 establishes that, until the first day of the fourth month following the publication of the common part of the IBS and CBS regulations:

- No penalties will be applied for the failure to record the IBS and CBS fields in tax documents;

- and the requirement for the exemption from the collection of IBS and CBS, provided for in Art. 348, § 1, of Supplementary Law No. 214/2025, will be considered fulfilled.

WHAT CHANGES AND WHEN

- Present

Adaptation period: the calculation of IBS and CBS in 2026 is purely for informational purposes, with no tax effects, provided that ancillary obligations are met

- 01/08/2026:

Deadline: mandatory completion of the new IBS/CBS fields in electronic tax documents. Non-compliant issuance will subject the taxpayer to legal sanctions.

- By 31/12/2026:

Collection of IBS and CBS is waived for taxpayers who comply with ancillary obligations (Art. 348, § 1, Supplementary Law 214/2025).

TAXPAYER PROTECTION IN 2026:

If a tax assessment notice is issued for non-compliance with an ancillary obligation related to the IBS/CBS, the taxpayer will have 60 days to remedy the omission identified by the tax authorities (Art. 348, § 3, Supplementary Law 214/2025, included by Supplementary Law 227/2026).

Timely compliance with the summons extinguishes the penalty imposed.

ATTENTION

The regulation published in April 2026 marks the beginning of the operational phase for IBS and CBS in electronic tax documentation.

For taxpayers, this requires immediate attention to the adaptation of internal systems and processes, especially since, as of August 1, 2026, issuance without the new fields will be subject to the penalties provided by law.

The content was produced by the SouzaOkawa Team. Use the Link above to access the (portuguese) PDF version