Joint Ordinance RFB/PGFN/MF No. 6/2026 has been published, regulating—within the scope of the Brazilian Federal Revenue Service (RFB) and the Office of the Attorney General of the National Treasury (PGFN)—the classification and treatment of habitual tax debtors, pursuant to Complementary Law No. 225/2026.

The regulation sets out objective criteria for identifying habitual non-compliance, establishes the applicable administrative procedure, defines defense and review mechanisms, and provides for significant restrictive measures applicable to taxpayers classified under this category.

Who may be classified as a habitual tax debtor?

Complementary Law No. 225/2026 introduced, for the first time at the national level, the concept of the habitual tax debtor, later regulated at the federal level by Joint Ordinance No. 6/2026.

This refers to a taxpayer (legal entity) whose tax behavior is characterized by substantial, repeated, and unjustified non-payment.

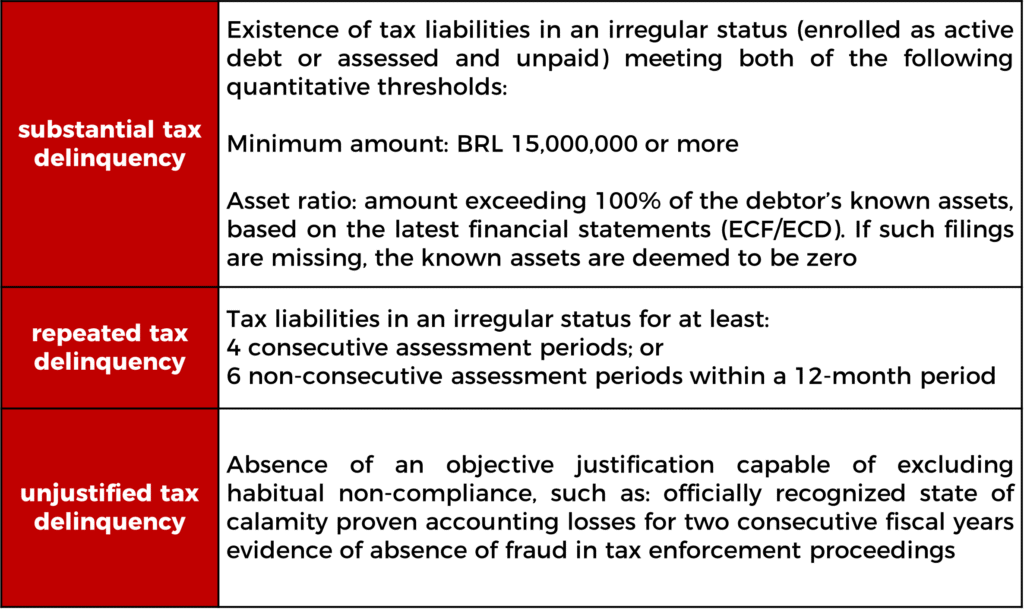

Cumulative qualification criteria

A taxpayer will be classified as a habitual tax debtor only if three requirements are met simultaneously.

Note: A tax liability is considered “irregular” when there are no known assets sufficient to cover the principal amount of the debt, or when there is no valid cause for suspension or regularization of its enforceability.

Deductions from the total tax liabilities

The Ordinance provides that certain tax liabilities should be excluded from, or deducted from, the calculation base used to determine habitual non-compliance, including those:

- subject to suspension of enforceability by court decision;

- enrolled as active debt with suspended enforceability;

- subject to deferral, installment plans, or tax settlements, provided payments are up to date;

- under dispute based on relevant and widespread legal controversy or subject to repetitive appeals;

- for which the law waives the requirement of guarantees.

Additional qualification scenario

A taxpayer may also be classified as a habitual tax debtor if it has already been held liable (administratively or judicially) and is a related party to:

- a company that has been dissolved or declared inactive in the past five years, with irregular tax debts of at least BRL 15 million; or

- a company already classified as a habitual tax debtor.

Due process and the right to defense are ensured, and the classification may be reviewed if the underlying liability decision is modified.

The Ordinance advances beyond the Complementary Law by restricting the application of related-party liability to cases where there is an effective attribution of tax liability linked to organizational or control relationships.

Administrative classification procedure

1. Jurisdiction

PGFN: when classification is based exclusively on federal tax debts enrolled as active debt;

RFB: when there are non-enrolled debts, or both enrolled and non-enrolled debts. In such cases, the RFB initiates the process, notifies the taxpayer, and forwards the case to the PGFN for awareness and comments.

2. Initiation of proceedings

The process begins with prior notice to the taxpayer, including the factual and legal grounds for potential classification.

Deadline: 30 days from notification to:

- regularize the debts (through full payment, negotiation, deferral, or proof of sufficient assets); or

- submit a defense.

3. Scope

The process may involve multiple related taxpayers, although the qualification criteria must be assessed individually, unless joint liability has already been established.

4. Defense

The defense must be based on objective criteria related to the grounds indicated in the notice. Important: The defense has suspensive effect, except in cases involving definitive findings of fraud, tax evasion, simulated corporate structures, participation in schemes to hinder tax collection, use or trade of illicit goods, absence at the tax domicile, or deliberate concealment of assets, income, or rights.

Effects of regularization

- Full payment: the proceeding is terminated;

- Full negotiation with regular payments: the proceeding is suspended.

2. Administrative appeal

If the defense is rejected, the taxpayer may file an administrative appeal within 10 days from notification of the decision.

2. Decision and review

Formal classification as a habitual tax debtor occurs when:

- the taxpayer fails to regularize its situation or present a defense;

- the appeal is not granted suspensive effect; or

- the defense is definitively rejected at the administrative level.

Once classified, the taxpayer will be included in a public list of habitual tax debtors, published on the Federal Revenue’s website and in the federal delinquency registry (Cadin).

Note: If the conditions persist, the taxpayer may request a reassessment upon demonstrating that the underlying causes have ceased.

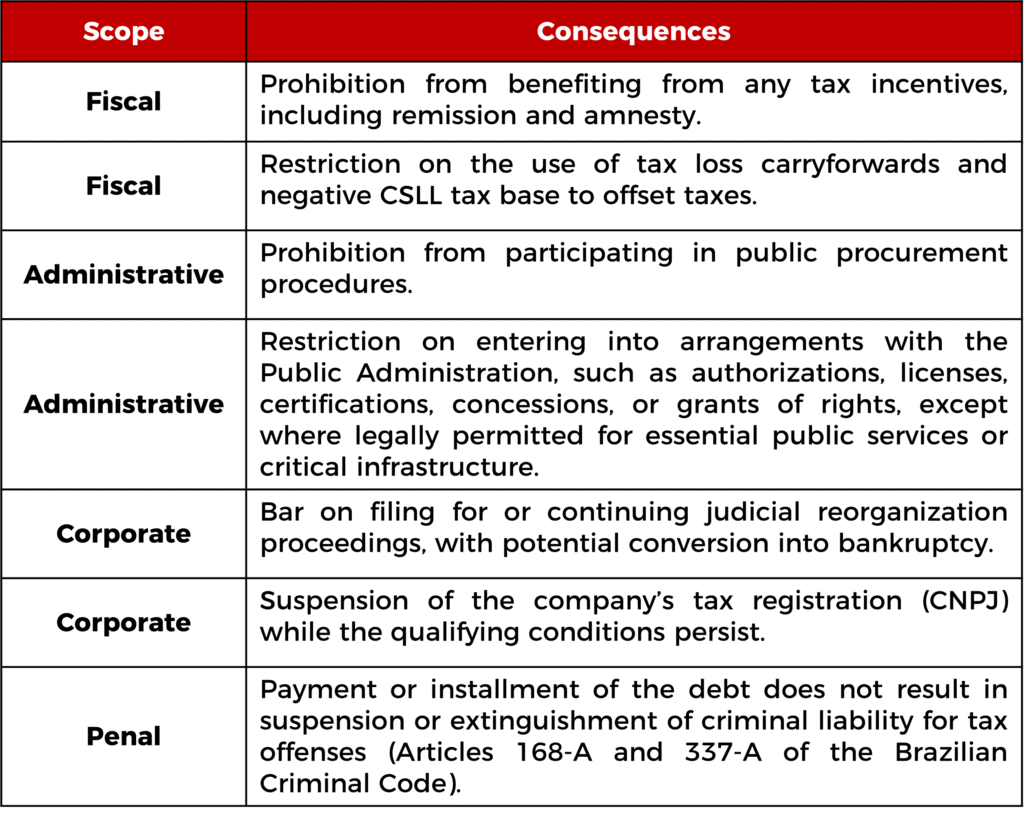

Penalties Applicable to Habitual Tax Debtors

Additional considerations

- Confia Program: taxpayers admitted to the program cannot be classified as habitual tax debtors while they remain enrolled;

- Sintonia Seal: will be automatically revoked upon classification.

Final remarks

Given the stricter regulatory environment, companies are advised to adopt preventive tax risk management measures:

- Liability mapping: conduct a comprehensive review of federal tax liabilities and assess proximity to qualification thresholds;

- Document organization: ensure accounting records (ECF, ECD), registrations, and contracts are fully updated;

- Tailored strategy: define a specific approach for each relevant liability, whether through installment plans, tax settlements, or administrative/judicial disputes;

- Governance and responsiveness: establish internal decision-making processes capable of responding quickly to preliminary notices.

Note: This content is for informational purposes only and does not constitute legal advice. Our team is available to assess your company’s specific situation, evaluate classification risks, and define the most appropriate strategy for regularization and defense.

This content is provided for informational purposes only and does not constitute legal advice. The application of this information depends on the analysis of each specific case.